On the same week the Government spent €100,000 publishing a report celebrating Ireland’s data centres, Irish households were told they had already paid €715 million to subsidise them. Welcome to Irish digital policy, where the numbers never quite add up the same way twice.

By Dr. Brian O’Donnell | Aurex Insights | June 2026

Ireland has become so accustomed to describing itself as a digital success story that it has almost stopped noticing what that success now costs. A country of just over five million people has built one of the densest data-centre clusters in the world – 89 active facilities mapped through 25 years of planning records, more than 40 in development, and roughly 129 centres listed across industry directories. That concentration is no longer a niche infrastructure story. It is a first-order question of industrial policy, electricity pricing, regional equity and political legitimacy. And after years of comfortable consensus, the questions are finally being asked in public.

This week they converged. Friends of the Earth published research arguing that Irish households have collectively paid an estimated €715 million extra in electricity bills to support data-centre expansion – roughly €360 per household at current levels. On the very same week, the Department of Enterprise published a report by KPMG, commissioned at a cost of €100,000, arguing that data centres have added €22 billion to the Irish economy since 2010, generated €2.8 billion in tax and support up to 876,000 jobs. Both reports are, in their own way, correct. Both are also partial. The critical task is to understand what each chooses not to count.

The Numbers the Government Can’t Dispute

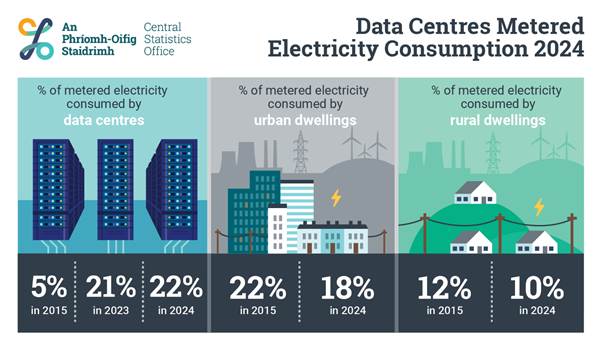

Start with the facts that are hardest to contest. According to the Central Statistics Office, data centres accounted for 22% of metered electricity consumption in Ireland in 2024, up from 21% in 2023 and just 5% in 2015. Their metered electricity use rose from 6,335 GWh in 2023 to 6,969 GWh in 2024 – a 10% increase in a single year – while consumption by all other metered users grew far more slowly. EirGrid’s median scenarios project data centres accounting for roughly 31% of national electricity demand by 2030.

For a country still heavily reliant on gas-fired generation, with climate targets it is already struggling to meet, and with a housing crisis that is simultaneously consuming political capital and construction labour, the implications of those numbers are serious. Ireland is not simply hosting servers. It has made a structural bet, largely unremarked in democratic debate, that one energy-intensive sector should be allowed to reshape the country’s electricity system, planning landscape and carbon trajectory.

The Minister’s Defence – and Its Limits

Peter Burke, the Minister for Enterprise, went on RTÉ’s Morning Ireland on 2 June to defend the sector and the Government’s report. His framing was confident: data centres are “a strategic opportunity for the Irish economy,” he said, employing around 19,500 people – split roughly 60% construction-related and 40% direct operational roles – and underwriting a green transition that will reduce emissions from 2030 onwards as offshore renewables come online.

These are reasonable points, honestly stated. But they raise as many questions as they settle. The 19,500 figure combines construction employment – which is temporary – with permanent operational jobs. Earlier government communications referenced around 1,800 direct roles. Industry-linked sources more recently cited approximately 16,000. Now the minister says 19,500, of which roughly 7,800 are direct. None of these figures is necessarily wrong. They are counting different things under the same headline. And when a government commissions a report for €100,000 explicitly to demonstrate sectoral value, and the minister then deploys that report’s figures in a morning radio interview the same day it is published, the public is entitled to ask whether it is receiving analysis or advocacy.

The green-transition argument also deserves scrutiny. The LEAP framework and CRU policy now require new large energy users to match at least 80% of annual electricity demand through new renewable generation. That is a meaningful condition. But it applies prospectively, to new connections, while the existing estate has accumulated without equivalent renewable matching obligations. And the promise that emissions will fall after 2030 is a projection about infrastructure that has not yet been built, financed by economic relationships that may or may not survive the next policy cycle. A hypothesis about a decade hence is not a defence of current pricing, siting and consent practices.

A €100,000 Report and a Pre-Decided Destination

This is the institutional point that most deserves scrutiny, and it is not made enough. Governments regularly commission research. There is nothing inherently improper about that. But there is an important distinction between commissioning an independent appraisal of costs, benefits, alternatives and distribution – and commissioning a report whose stated aim is to demonstrate the economic value of a sector whose expansion the commissioning minister has already announced. The KPMG report, to be fair to it, is a competent piece of ecosystem analysis. What it is not is a net benefit assessment. It does not seriously grapple with the electricity costs being borne by other users, the opportunity cost of diverting grid capacity from other uses, the regional concentration of physical burdens, or the employment quality of direct versus construction roles.

That gap matters because the public debate is being conducted as if the KPMG findings settle the question. They do not. They reframe it. And the framing – 876,000 jobs, €22 billion in cumulative GVA, €2.8 billion in tax – is designed, consciously or not, to make the costs seem trivial by comparison. A serious democratic debate about digital infrastructure policy requires better than that.

What Friends of the Earth Gets Right – and Where It Stops Short

Friends of the Earth’s €715 million household cost estimate is an advocacy figure, and it should be labelled as such. The precise euro amount depends on modelling assumptions about cost allocation, counterfactual demand and tariff design that reasonable analysts can dispute. The organisation is not a neutral economic research body, and its report is structured to support a policy conclusion – a moratorium on further data-centre connections – that goes beyond what the evidence alone demands.

But directionally, the argument is sound. Ireland’s electricity cost recovery works by socialising system costs across all metered users. If one sector is responsible for a disproportionate share of marginal demand growth – and it demonstrably is – then other users inevitably absorb some of the associated investment costs unless explicit ring-fencing prevents it. The CRU has moved in this direction with its new conditions, but those conditions apply going forward. The existing cost accumulation is real, it is already in households’ bills, and no amount of argument about future renewables reverses what has already been paid.

What does that gap actually cost?

The precise figure is harder to pin down than advocates on either side acknowledge. Households pay approximately 31.7c/kWh for electricity including all taxes, while very large commercial users – a category that includes most data centres – pay around 19.5c/kWh excluding VAT, according to SEAI’s official January–June 2025 figures.

That differential reflects a combination of factors: tax treatment, buying structure, and network tariff design. Whether it constitutes a household “subsidy” to data centres is a question of regulatory philosophy as much as arithmetic. The Friends of Earth estimate of €360 cumulative per household between 2015 and 2023 is the most cited figure, but it rests on modelling assumptions that the industry disputes – and that a neutral analyst should treat as indicative rather than definitive.

What is not in dispute is the structural reality: Ireland’s electricity cost recovery socializes system costs across all metered users. When one sector drives a disproportionate share of marginal demand growth and pays a lower effective rate per unit, the pressure on other users’ bills is real – even if the exact quantum remains contested.

The Geography of Inequality

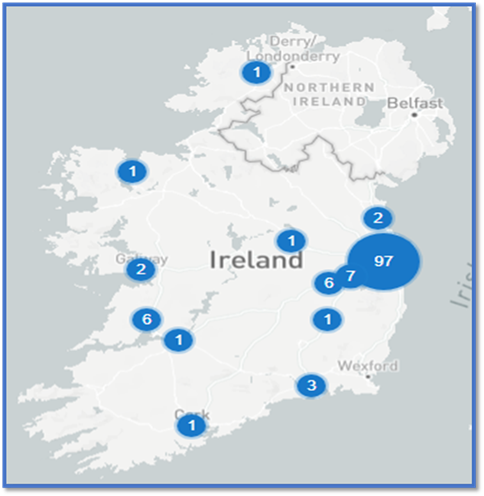

Of all the facts in the current debate, the most politically underexplored is the one produced by TASC, the independent think-tank: 97 active or planned data-centre buildings in the greater Dublin area, of which 84 – nearly 90% – are located in areas classified as marginally below average, disadvantaged or very disadvantaged on the Pobal HP deprivation index. Clusters in Blanchardstown, Clondalkin and Tallaght are the most visible examples.

The business logic is banal: cheaper land, simpler planning, proximity to substations, fibre routes and ring roads. The political logic is far more troubling. Communities that have already seen decades of underinvestment in schools, transport, healthcare and social infrastructure are now being asked to host the physical back-end of a global digital economy whose gains flow mostly to shareholders in Seattle, Cupertino and Amsterdam.

Ireland has no mechanism for community benefit agreements equivalent to those increasingly used in wind energy development in rural areas. There is no transparent model by which the communities that house hyperscale facilities receive a share of the business rates, a negotiated amenity fund or any formal acknowledgement that they are providing something of national strategic value. That is a governance failure, and it will not age well.

What Genuine Data Centre Policy Requires

The true test of a serious industrial policy is not whether the government can identify a winning sector. It is whether the government can honestly price the bets it is making on behalf of citizens who did not ask to be venture partners. By that standard, Irish data-centre policy has not yet cleared the bar.

A serious policy framework would require at minimum:

First, a publicly maintained national registry of operational, approved and in-development data centres – not assembled by investigative journalists from 25 years of planning files, but maintained as a public resource by the state that issues the planning permissions.

Second, disaggregated employment reporting: permanent operational roles, specialist contractor positions, temporary construction jobs and the wider digital economy that uses cloud services must be counted separately. Conflating them does not generate better policy; it generates better press releases.

Third, a genuine distributional account of network and system costs: who is paying for grid reinforcement, capacity reserves and fossil back-up, and whether large energy users are contributing proportionately to those costs.

Fourth, a community dividend mechanism: if data centres are genuinely strategic national assets sited in specific communities, those communities should receive an explicit and transparent share of the value.

Fifth, a renewable additionality standard applied retrospectively, not only to new connections: the existing estate should be on a credible transition pathway, not simply grandfathered under legacy conditions while new entrants face tighter rules.

The Question Ireland Can No Longer Avoid

Ireland still has time to build a coherent digital infrastructure strategy – one that recognises data centres as genuinely useful, that takes EU AI sovereignty seriously as a policy objective, and that also acknowledges that useful infrastructure built on invisible subsidies and unpriced spatial inequality is not a strategy. It is a deferral.

The data-centre debate has returned to the headlines because it has escaped the server room and entered ordinary life: electricity bills, planning disputes, stretched grids, communities that feel overlooked and a climate plan that keeps slipping. The government’s response – a morning radio interview, a commissioned report and a large number – is not wrong, exactly. It is just not enough.

Ireland’s data centres are not going away, nor should they. But the country cannot continue to describe an unpriced power subsidy for a narrow slice of the global economy as a national strategic vision. At some point – and that point is now – the state must tell citizens what the full cost is, who is paying it, who decided that was acceptable, and what they got in return.

That is not an anti-technology argument. It is the basic minimum of democratic accountability. And on that measure, the €100,000 report published this week does not even begin to answer the question.

Ireland’s data-centre policy will continue to look less like industrial strategy and more like an unpriced power subsidy dressed up as inevitability – until the state is willing to count the full cost, not just the parts that make a good press release.

Dr. Brian O’Donnell is Principal of Aurex Insights. He writes on political economy, public policy and strategic affairs in Ireland and Europe.

www.aurexinsights.com

© Aurex Insights 2026. Published for public policy purposes. Reproduction with full attribution permitted.

Sources

- CSO – Data Centres Metered Electricity Consumption 2024 (June 2025)

- The Journal Investigates – Ireland’s Data Centres: A 25-Year Planning Record (June 2025)

- TASC – Data Centres and Deprivation in Greater Dublin (May 2026)

- Friends of the Earth Ireland – The Cost of Data Centre Growth in Ireland (May 2026)

- KPMG / Department of Enterprise – The Value of Data Centres to Ireland (June 2026); commissioned at a cost of €100,000

- RTÉ News – Data Centres a “Strategic Opportunity” – Minister Burke (2 June 2026)

- Oireachtas Library & Research Service – Research Matters: The Future of Data Centres in Ireland (March 2025)

- TechPolicy.Press – What Ireland’s Data Center Crisis Means for the EU’s AI Sovereignty Plans (December 2025)

- EirGrid – Tomorrow’s Energy Scenarios 2024

- DataCenterMap – Ireland Data Centers (accessed June 2026): 129 centres listed across 13 markets

- GridBeyond / Department of Enterprise – Large Energy User Action Plan (LEAP) (January 2026)

- Bloomberg – Ireland Wants to Get Back AI Data Centers (January 2026)

Map analysis: Aurex Insights, based on The Journal Investigates, TASC, Oireachtas Library & Research Service, DataCenterMap and CSO. Indicative only – not an official state registry.