Why a debtor balance sheet, runaway current spending and a one‑third dependence on US multinationals should worry Irish policymakers

By Dr. Brian O’Donnell | Aurex Insights | May 7, 2026

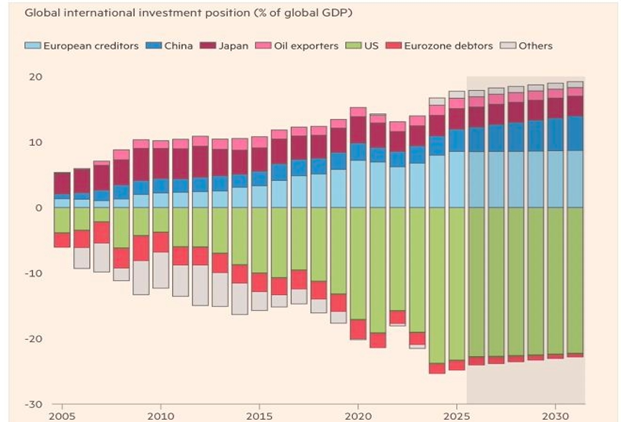

A recent Financial Times analysis on global imbalances made me stop and think again about Ireland’s position in the world economy. Not because Ireland is named directly in the chart, but because the forces it describes – persistent surpluses in some economies, rising indebtedness in others, weak domestic demand in major surplus countries, and the growing risk of disorderly adjustment – speak directly to the vulnerability of small, highly open economies like Ireland.

The central warning is stark: the chances of preventing the next financial crisis through coordinated action are “close to zero,” and policymakers must instead prepare for crisis. That warning matters for Ireland because the country does not need to sit at the centre of the chart to be caught in the eventual adjustment.

A piece published here in late April described what lies beneath Ireland’s headline surpluses: a fiscal strategy that plans to spend five out of every six euros of corporation tax receipts between now and 2030 on day-to-day spending and permanent tax measures, while saving only a fraction for the Future Ireland Fund and related vehicles. That, on its own, is a serious structural concern. But once you place it inside today’s global map of creditors, debtors and widening imbalances, the picture becomes harder to look away from.

The logic of spending five in every six euros of a windfall might be defensible if that money were being deployed efficiently, if outcomes were improving at pace, and if the State were demonstrably building long-term capacity and resilience. But that is not what the evidence shows. What we are seeing instead is 2026 spending growth running at 9.3% against an underlying tax base growing at 3.7%, a Department of Education overspend of between €600 million and €700 million being quietly absorbed by raiding other departmental budgets, and a pattern of annual overruns across government that has become normalised rather than corrected. Five in every six euros of a once-in-a-generation windfall is being spent, and a growing share of it is not building a stronger Ireland – it is being absorbed into an expanding and under-accountable spending machine that will be very difficult to unwind when the cycle turns.

That is the domestic skeleton. This article is the global X-ray. The question it asks is straightforward: how exposed is Ireland when today’s global imbalance story – US indebtedness, entrenched surplus blocs, rising protectionism and concentrated tax flows – is put alongside Ireland’s own fragile fiscal model?

What the chart is really showing

The FT chart (below) is not just an illustration; it is effectively a compressed version of IMF work on net international investment positions by country blocs. It shows how a small group of creditor economies has accumulated ever-larger claims on the rest of the world, while the United States has become the system’s dominant debtor.

The largest negative block in the chart (above) is the United States. By the end of 2025, the US net international investment position had fallen to -$27.54 trillion, with foreign assets of $42.96 trillion against liabilities of $70.49 trillion. The IMF found that the recent widening in global debtor positions was entirely accounted for by the US, whose net international investment position (NIIP) – the value of all foreign assets owned by residents of a country minus the value of that country’s assets owned by foreigners – deteriorated by 3.6 percentage points of world GDP in 2024 alone. In the FT chart, that translates into the US moving towards roughly -23% of global GDP by 2030.

On the creditor side, the chart stacks together European creditors, China, Japan and oil exporters. The euro area as a whole held €1.43 trillion in net external assets by mid-2025, equal to 9.3% of euro-area GDP, while also running a current account surplus of 2.1% of GDP. Add Japan, China and oil exporters, and the positive side of the chart climbs towards roughly +20% of world GDP by the end of the projection period.

That matters because this is not just about trade balances in a single year. These are accumulated stock positions. A world in which one country keeps absorbing excess savings and several creditor blocs keep accumulating claims is a world that becomes progressively more fragile financially.

Ireland’s hidden exposure disappears in the aggregation

The most important point from an Irish standpoint is that Ireland is not separately identified in the chart. Instead, the IMF’s underlying framework places countries into broader categories such as European creditors and European debtors.

That distinction is critical. The IMF explicitly classifies Ireland alongside Cyprus, Greece, Italy, Portugal and Spain as part of the European debtor group. Eurostat’s latest country-level data show that France, Spain and Ireland had the largest net external liabilities in the EU in 2023, with Ireland’s NIIP standing at -€304 billion at end-2025, placing it firmly on the debtor side of the European ledger. So while the public conversation often treats “Europe” as a homogeneous surplus bloc, Ireland is in fact one of the EU’s largest debtor countries on the underlying external balance-sheet data.

This is the first major lesson from the chart. Ireland may visually disappear inside a European category, but economically it sits on the vulnerable side of the ledger.

Ireland’s own balance sheet is still highly exposed

Ireland’s more recent net international investment position remains deeply negative. By late 2025, Ireland’s NIIP stood at roughly -€304 billion, about -76% of GNI*, even after a substantial improvement from earlier crisis-era extremes.

This is the paradox. Relative to distorted GDP figures, Ireland can sometimes look safer than it really is. Relative to modified GNI*, and once multinational balance-sheet effects are properly considered, the country remains highly exposed. Ireland’s foreign assets and liabilities are both enormous because multinational structures and financial flows dwarf the domestic economy. That means stability can look convincing right up to the point where external conditions shift abruptly.

The surplus headlines are real, but they do not settle the question

Ireland’s public finances look strong on the surface. The original Budget 2026 surplus projection of €5.1 billion has since been revised up to about €9.2 billion (2.5% of GNI*), while the 2025 surplus also came in stronger than expected. The debt ratio is forecast to keep falling, with gross debt projected at 58.6% of GNI* in 2026, down from 61.7% in 2025.

These are real improvements. But they do not settle the argument, because the underlying position is weaker than the headline suggests. Independent Budget 2026 analysis estimates that once windfall corporation tax receipts are stripped out, Ireland runs an underlying deficit of €13.6 billion, or 3.8% of GNI*, in 2026. That means temporary revenue strength is being treated as if it were permanent fiscal capacity.

This week’s IFAC warning sharpens the concern

The headline numbers have since been confirmed in granular detail. This week’s fiscal monitor from the Irish Fiscal Advisory Council (IFAC) provides the department‑by‑department evidence that moves the argument from assertion to documentation.

The details are revealing. Current spending in health, children and social protection is up by more than 10% on last year, while education spending is up 8.6%. Yet tax receipts excluding corporation tax are up only 3.7% so far this year. On top of that, the Department of Education is already projecting an overspend of between €600 million and €700 million in 2026, following additional top‑ups of €580 million and €1.09 billion in the previous two years; other departments are now being told they will have to cut their own budgets to bail it out.

This is no longer a story of one‑off slippage. Overruns of €4 – 5 billion across government have become routine in recent years, funded in large part by volatile corporation tax receipts, and IFAC has warned that this pattern is eroding the credibility of the budget process itself. Spending is running far ahead of the underlying tax base, and the gap is being bridged by windfalls and by comfort taken from headline surpluses. Economically, that is poor management of scarce public resources: it is pro‑cyclical, it confuses temporary and permanent revenues, and it risks hard‑wiring a permanently larger spending base into a system that still lacks clear accountability for outcomes, delivery or value for money.

What high debt means in Ireland even when ratios look manageable

Ireland’s debt burden can look manageable when measured against headline GDP, but that can be dangerously reassuring. GDP in Ireland is heavily inflated by multinational activity that does not fully reflect the tax base or resource base available to service public debt. That is why debt relative to GNI* is the more meaningful benchmark.

On that measure, the picture is better than during the crisis, but still not trivial. General government debt is forecast at around 58.6% of GNI* in 2026, having fallen sharply from close to 170% in 2013. That is a major improvement. But it still means the Irish state carries a substantial debt stock while also depending on an unusually volatile and concentrated tax base.

So what does “high debt” mean in practice, even if the ratio looks manageable? It means the State has less room to absorb a major shock without renewed borrowing or painful retrenchment; debt-service costs can rise again over time; and if windfall revenues weaken, the ratio can deteriorate faster than headline measures suggest. The real issue is not whether today’s ratio looks respectable. The issue is whether the income base behind it is durable.

Borrowing to save: a strategy with risks

This is where the government’s new strategy becomes harder to defend. Ireland is building long‑term savings vehicles such as the Future Ireland Fund and the Infrastructure, Climate and Nature Fund, while at the same time continuing to issue debt and carry a sizeable public balance sheet. In principle, parking windfall revenues in sovereign funds is good economics: exceptional corporation tax receipts will not last forever, and part of today’s windfall should be converted into future resilience. But the State now plans to save only about one euro in every six of corporation tax receipts between now and 2030, while allowing the other five to flow into day‑to‑day spending and tax cuts.

The strategy becomes much more questionable once it amounts to borrowing while saving. Central Bank financial accounts show Irish government debt rising to around €199.8 billion in late 2025, up roughly €10.4 billion in a single quarter, even as government financial assets also climbed, largely through purchases of debt securities. In other words, the State is issuing sovereign liabilities on one side of the balance sheet and buying financial assets on the other, while the NTMA continues to manage a substantial stock of debt to maintain market access and liquidity.

Under very disciplined conditions that can be justified. But it carries clear dangers. It can create a false sense of strength if headline assets grow while the underlying budget remains structurally weak. It can amount to borrowing at sovereign rates to build a financial portfolio instead of first fixing the structural deficit and domestic capacity constraints. And it can make it politically easier to ratchet up current spending by pointing to the existence of a savings fund, even though the overall fiscal stance is still pro‑cyclical and still heavily dependent on a narrow, volatile tax base.

A bigger danger: the state’s growing dependence on corporation tax

The biggest medium-term vulnerability may be even simpler. Ireland is building more and more of the State on a highly concentrated, highly internationalised corporation tax base. Department of Finance projections indicate corporation tax receipts could rise to €45.1 billion by 2030. International data on large MNC corporation tax per capita place Ireland in the very top tier globally, alongside Luxembourg and a small group of coordination‑centre jurisdictions. In other words, Ireland is not just highly dependent on corporation tax in aggregate; on a per‑person basis it is one of the most intense large‑MNC tax collection points in the world.

The way Ireland got here has been unusual. From the mid‑2010s to the early 2020s, corporation tax receipts grew at an average rate of a little over 20% per year, an extraordinary pace for a mature tax head, before growth began to stabilise more recently. Over roughly a decade, CT receipts have risen several‑fold, helping to double total tax revenues between 2014 and 2024, and by 2025 corporation tax was contributing almost one‑third of all Exchequer tax receipts, with annual CT now close to €33 billion.

That explosion reflects specific structural drivers rather than a broad‑based strengthening of the domestic tax base. Major US technology companies have onshored large intellectual‑property portfolios into Ireland, computer‑services exports have soared from about €32 billion in 2012 to almost €196 billion in 2022, and CT payments from the chemical and pharmaceutical sector alone more than doubled from €2.65 billion in 2021 to €5.54 billion in 2022.

That is not just a large number. It is a dangerous concentration. The Irish Fiscal Advisory Council estimates that the top three corporate groups accounted for 46% of all corporation tax revenues in 2024, roughly €13 billion, while the top ten accounted for almost 60%. Separate IFAC work estimates that US multinationals account for around three-quarters of all corporation tax receipts in Ireland.

That means the Irish State’s medium-term spending and saving plans are increasingly tied to the profitability, booking decisions and tax behaviour of a tiny number of largely US-owned firms. It also means Ireland is unusually exposed to any combination of US tax reform, reshoring pressure, tariff escalation, weaker global demand, sector-specific profit reversals, or renewed international tax coordination.

This is what makes the current strategy especially risky between now and 2030. At the top is concentration risk: a small number of groups pay a very large share of total CT. Beneath that sit firm‑level risk (the performance or strategic decisions of one or two firms can move the aggregate), footloose‑industry risk (highly mobile activities can be rebooked in other hubs), and infrastructure and housing risk (bottlenecks in capacity undermine Ireland’s attractiveness for new investment). Underpinning all of this is international tax reform risk: changes such as the OECD’s Pillar One, which reallocates some profit to sales markets, and potential US tax or tariff shifts could reduce the amount of taxable profit booked in a small domestic market like Ireland, especially if IP assets are offshored again.

This is not prudence. It is concentration risk disguised as fiscal strength.

Historical patterns: who ends up adjusting?

The historical record suggests large imbalances usually unwind in one of two ways. When imbalances are accompanied by protectionism and retaliation, it is often the surplus economies that are hit hardest. The United States in the 1930s and Japan in the 1980s entered the adjustment phase as surplus powers and then suffered deep, prolonged economic pain when the external model could no longer be sustained.

When imbalances unwind without a major protectionist surge, it is usually the deficit economies that are forced to adjust. Latin America in the debt crises of the 1970s and 1980s, East Asia in 1997-98, and peripheral Europe after 2008 are all examples of debtor countries absorbing the pain when financing conditions turned.

Today’s environment looks worryingly closer to the first pattern in one respect: protectionism is rising again, especially from the main deficit economy, the United States. But Ireland is exposed under either pattern. If surplus countries are hit, the profits and tax flows from the multinational sector could weaken sharply. If debtor countries are forced to adjust again, Ireland remains on the vulnerable side of the European balance sheet.

The opportunity Ireland may be missing

The deeper strategic question is whether Ireland has used the windfall years to become more resilient, or just more expensive. Since 2016, the State has benefited from exceptional corporation tax flows, creating a rare chance to build buffers, support indigenous enterprise, diversify exports, and deepen productive capacity.

Germany’s experience in the 2008-09 crisis is relevant here. Research shows that owner-managed Mittelstand firms (Irish equivalent of SMEs) were significantly more stable through the Great Recession than non-Mittelstand firms. That does not mean Ireland can copy Germany mechanically. But it does underline a strategic point: resilience comes from depth, diversity and productive domestic capacity, not simply from strong headline receipts.

Ireland had a chance to use windfalls to strengthen SMEs, capacity and fiscal resilience. Instead, this week’s IFAC data suggest the system is still defaulting to fast current spending growth.

A call for reflection before crisis forces it

The FT chart is useful not because it tells Ireland’s story directly, but because it shows the world Ireland is operating in. One giant debtor, several entrenched creditor blocs, and growing stock imbalances that make the global economy more financially brittle.

Against that backdrop, Ireland is not the comfortable European creditor it may appear to be in broad-brush commentary. It is a country with one of the largest net external liability positions in the EU, a still-material debt burden relative to GNI*, a structural deficit beneath the surplus headlines, and a fiscal model that is becoming increasingly dependent on a very narrow corporation tax base dominated by US multinationals.

That does not mean crisis is inevitable. It does mean the warning lights are flashing.

Dr. Brian O’Donnell is the founder and principal of Aurex Insights, an independent public policy, economic and legislative strategy practice working between Ireland and Canada.