Europe is more dependent on LNG than ever; Canada now has one last chance to turn energy from a domestic argument into a strategic capability.

By Dr. Brian O’Donnell | Aurex Insights | May 28, 2026

In the last decade Canada managed a rare feat in global energy politics: it sat on one of the world’s most attractive resource bases and still convinced investors it was not serious about being an energy power. Big export projects died in regulatory thickets. Timelines stretched, costs rose, and allies quietly turned to other suppliers. Meanwhile, the United States and Qatar locked in long-term LNG contracts around the world, including in Europe. Canada’s debate stayed stuck on a binary: hydrocarbons versus climate.

That frame no longer fits. A new federal government in Ottawa, a second major Middle East shock in four years, and Europe’s uneasy dependence on a small group of gas suppliers have rewritten the script. Energy is no longer simply a domestic environmental issue or a provincial grievance. It is now a question of statecraft, industrial strategy and long-run competitiveness.

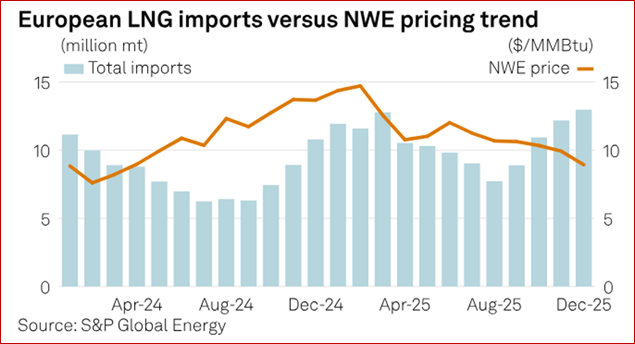

This week’s LNG agreement between Canada and Germany’s state-owned utility SEFE is a marker of that shift. On the surface, it is modest: SEFE has agreed to buy 1 million tonnes per year of LNG for 20 years from the planned Ksi Lisims export terminal in British Columbia, with deliveries expected from 2030. Ksi Lisims itself is designed as a 12 million tonne-per-year floating LNG project, making the German contract strategically meaningful even if it does not yet fill the facility. Against a European gas market that imported record LNG volumes in 2025 and is expected to remain heavily reliant on seaborne gas in 2026, that volume is small. What matters is not the tonnage but what it signals: Canada intends to treat energy as a strategic export again.

In 2025, Europe’s LNG imports rose by 27%, and the United States supplied 77.53% of those volumes, up from 57.64% in 2024, according to S&P Global data cited by market reporting. In the first quarter of 2026, LNG accounted for 62% of total European gas imports, up from 58% in 2025, while U.S. LNG still accounted for 63% of Europe’s LNG imports. That is the real backdrop to the Canada–Germany deal: Europe has reduced its dependence on Russian pipeline gas, but it has replaced it with a deeper dependence on globally traded LNG and a narrower set of suppliers.

The chart captures the broader point. Europe is no longer dealing with the acute scarcity of 2022; it is dealing with a structurally LNG-heavy system in which price signals, shipping routes and geopolitical disruptions determine where marginal cargoes go. Canada’s opportunity lies inside that new system, not outside it.

How Canada Handicapped Itself

Canada’s current LNG moment is not emerging from a vacuum. It follows roughly ten years of self-imposed delay.

Regulatory regimes for major projects were repeatedly rewritten. Political narratives oscillated between welcoming capital and portraying new fossil infrastructure as incompatible with climate commitments. Investors heard tax credits and innovation incentives on one side, but also saw cancelled pipelines, contested approvals and prolonged uncertainty on the other.

The result was predictable:

- Capital flowed more readily to U.S. Gulf Coast projects and to established Middle Eastern exporters.

- Canada gained a reputation as a place where large projects are possible, but unusually slow, politically fragile and procedurally complex.

- The strategic advantage of having a large, relatively low-carbon hydrocarbon base inside a stable democracy was undercut by execution risk.

That pattern is not unique to Canada. Several OECD economies have struggled to align climate goals, local politics and major energy infrastructure. But for a country with Canada’s resource endowment, hydroelectric base and institutional capacity, it has been an expensive own goal.

A New Government, a New Frame

The shift under the Carney government is less about one LNG contract than about how energy is now being framed.

Instead of debating in the abstract whether gas exports are “compatible” with climate policy, the conversation has shifted to more concrete questions:

- Which projects can be built with acceptable Indigenous and local consent?

- Can facilities be electrified or designed to have materially lower upstream emissions than the global average?

- How do specific exports fit into a pathway where domestic emissions fall while partner countries reduce dependence on coal, Russian gas or higher-carbon supply?

Under that framing, selected LNG and energy projects are being presented as industrial policy and energy security policy, not as departures from climate strategy. The implicit story is that Canada will support a limited number of strategically important, lower-emissions projects that strengthen allies, crowd in capital and anchor supply chains, rather than simply chasing maximum volume.

That is a more coherent proposition for investors, allies and domestic voters. It is also more realistic. Canada cannot dominate LNG markets. It can, however, compete for a valuable niche.

Canada’s Competitive Edge: Narrow but Real

Canada cannot out-compete the United States or Qatar on sheer LNG volume. Its edge sits elsewhere.

Political reliability. In a world of repeated supply shocks and sanctions risk, long-dated contracts from a politically stable, rule-of-law democracy carry a premium. For European buyers burned by over-reliance on a small number of suppliers, diversification is no longer an abstract policy goal. It is a commercial necessity.

Cleaner upstream molecules. With abundant hydroelectricity and a strong environmental regulatory base, Canada can design projects with upstream emissions intensities well below the global LNG average. That matters in a world of tightening carbon rules and investors scrutinising operational emissions. If Europe is going to keep some gas in the system through the 2030s and perhaps into the 2040s, it will prefer cleaner molecules to dirtier ones.

Institutional and financial depth. Canada has a mature financial sector, credible public institutions and the capacity to de-risk parts of the value chain without turning each project into an open-ended fiscal liability.

Scope for broader industrial policy. LNG alone is not a strategy. But LNG linked to Indigenous equity participation, local manufacturing, port and transmission infrastructure, and pathways into hydrogen, critical minerals and clean-tech deployment can form part of a coherent industrial play.

These advantages are specific. They do not justify a rush to build every proposed export project. They do justify a strategic, limited portfolio of projects that align with Canada’s long-term economic and diplomatic interests.

Europe’s Energy Problem Is Changing, Not Disappearing

On the European side, the story is subtly different from the emergency of 2022. Europe has diversified away from Russian pipeline gas, built new regasification capacity at speed, and accelerated efficiency and renewables. LNG regasification capacity increased by almost a third between 2021 and 2025, although the build-out slowed markedly last year.

The map of Europe’s LNG regasification terminals is a reminder of how thoroughly the continent’s gas geography has changed. What was once a system organised around major pipeline corridors is now increasingly a network of ports, floating regasification units and coastal terminals stretching from Iberia and the UK to the Baltics and the Mediterranean.

Yet this is not a simple success story. Europe’s gas consumption fell by 19% between 2021 and 2024, then rose by 3% between 2024 and 2025 because of colder weather and weaker renewable output. Independent analysis now suggests gas consumption could fall by a further 14% between 2025 and 2030, with LNG demand down by roughly 23% over the same period, and by 29% in the EU itself, if current policy trajectories hold. In other words, Europe still needs gas security, but inside a shrinking market.

This is also where the geography of the Canada–Germany deal is often misunderstood. Very little of this gas may ever travel physically from British Columbia to Germany. In a global LNG market, portfolio players optimise cargoes through swaps: Canadian west-coast volumes can move into Asian demand, while Atlantic cargoes from the U.S. Gulf Coast or elsewhere can be redirected into Europe against the German contract. The economic significance of the SEFE deal therefore lies less in the literal shipping route than in the willingness of a major European buyer to underwrite Canadian-linked LNG volumes for two decades as part of its diversification strategy.

That is why the perennial Canadian argument that gas should simply be piped east for Atlantic export, while politically intuitive, is incomplete. East-coast LNG faces its own pipeline constraints and cost disadvantages, while the global LNG trade already solves part of the geography problem through portfolio trading and swaps. The real constraint is not geography alone. It is Canada’s ability to get credible projects financed, permitted and built.

This is where Canadian energy matters less as a “saviour” and more as a hedge.

- European buyers do not need Canada to replace all lost Russian volumes. They do need contracts that diversify risk across suppliers, routes and emissions profiles.

- Long-dated arrangements with a politically reliable, lower-emissions producer can support the portion of Europe’s gas demand that persists into the 2040s, even as overall volumes fall.

- For Europe, the main pitfall is locking into more gas than is consistent with its own climate law. For Canada, the pitfall is investing in capacity that arrives just as demand fades faster than expected.

The strategic sweet spot is limited, flexible volumes that fit inside a declining European gas trajectory while providing predictable cash flows for Canadian projects.

More Deals – But Not Unlimited Ones

Will more Canada–Europe LNG deals be signed? Very possibly, but not in an indiscriminate wave.

The commercial logic is there. Europe’s dependence on LNG deepened further in early 2026, and the Middle East shock has reminded buyers that concentration risk remains real. Qatar supplied only 6% of Europe’s LNG imports in the first quarter of 2026, but the March attack on Ras Laffan and the effective closure of the Strait of Hormuz showed how even a relatively small share of supply can matter if disruptions persist. For buyers in Germany, Italy or elsewhere, a long-dated contract from Canada is valuable not because it transforms Europe’s balance on its own, but because it adds resilience to a system that remains vulnerable.

But Europe does not need unlimited new gas. Forecasts suggest Europe’s LNG imports may peak around 2027 before easing through the rest of the decade. That means additional contracts are more likely to go to a narrow set of projects that can demonstrate three things at once: reliable delivery, acceptable emissions intensity and credible execution. The relevant question is not whether Canada can sign many deals. It is whether it can sign the right ones.

The Next Two Decades: Execution, Timing, and Transition

Thinking like a macroeconomist, there are three distinct horizons.

1–5 years: Execution risk

The near-term challenge is to get a small number of flagship projects from rhetoric to reality.

- Do approvals and permitting actually move faster under the new policy stance?

- Are Indigenous partnerships structured in ways that are legitimate and durable?

- Can Canada keep projects on time and on budget in a tight global construction market?

This is the phase where Canada either changes its reputation as a slow, uncertain place for large projects – or confirms it.

5–10 years: Market positioning

By the early to mid-2030s, global LNG supply will almost certainly be much larger than today. Canada will be competing in a looser market where price, reliability and carbon intensity all matter.

- If Canadian projects deliver genuinely lower upstream emissions and strong reliability, they can capture a premium segment of demand from buyers under pressure to decarbonise and diversify.

- If they do not, they risk being squeezed between cheaper producers and falling demand.

At the same time, European gas demand will be lower. Contracts signed now must be flexible enough to accommodate that reality.

10–20 years: Transition credibility

Beyond the 2030s, the question becomes whether Canada uses this energy window to build a broader competitive position.

- Does LNG revenue help finance investment in clean electricity, grid upgrades, critical minerals and zero-carbon exports?

- Or does Canada end up with stranded assets and a delayed transition, having treated LNG as an end in itself rather than a bridge?

The answer will determine whether today’s second chance at energy statecraft is a genuine pivot or simply a better-packaged version of the old model.

Pitfalls to Avoid

There are several obvious risks.

- Over-promising to everyone. Portraying each project as simultaneously transformational for regional economies, climate-neutral and geopolitically indispensable invites disappointment.

- Assuming Europe’s demand story. Betting on volumes that are inconsistent with EU climate law, or underestimating the speed of efficiency and electrification, is a recipe for underused capacity.

- Neglecting domestic social licence. Under-investing in credible environmental safeguards and Indigenous partnerships would re-create exactly the conflicts that slowed Canada down before.

- Treating energy as separate from productivity. Export molecules matter, but so do the manufacturing, services, innovation and infrastructure ecosystems built around them.

A New Chapter, If Canada Chooses It

Canada has spent much of the last decade talking about missed opportunities in energy. The combination of a new federal stance, a more serious industrial-policy mindset, and Europe’s continuing – if changing – security needs creates something closer to a second chance.

It is not a chance to dominate global gas markets. It is a chance to demonstrate that a resource-rich democracy can align energy security, climate constraints and industrial policy in a way that serves both its citizens and its allies.

Whether that becomes Canada’s new comparative advantage – or another footnote in a long story of ambivalence – will depend less on announcements than on decisions taken, or ducked, in the next five to ten years. The SEFE–Ksi Lisims deal will either be remembered as the moment Canada stopped treating energy as a domestic argument and started treating it as a strategic capability, or as another missed inflection point.

Dr. Brian O’Donnell is the founder and principal of Aurex Insights, an independent public policy, economic and legislative strategy practice specialising in enterprise policy, industrial strategy and fiscal analysis, working between Ireland and Canada.