Inside Carney’s first Spring Economic Update and the new Canada Strong Fund – and what Norway, Singapore, Ireland and Kuwait teach us about turning big fiscal bets into genuine public wealth.

By Dr. Brian O’Donnell | Aurex Insights | April 30, 2026

This week, Canada’s first year under Prime Minister Mark Carney closed with the most revealing announcement of his premiership so far: the launch of the Canada Strong Fund, Canada’s first national sovereign wealth fund. On April 28 – the exact one‑year anniversary of the election that brought him to power – Finance Minister François‑Philippe Champagne tabled the Spring Economic Update, anchored by the launch of the Canada Strong Fund: billed as Canada’s first national sovereign wealth fund and the financial engine behind a new wave of energy and infrastructure projects. The timing is almost too neat. On the anniversary of his mandate, Carney has planted his flag on the one piece of economic architecture that most clearly defines his brand – the federal balance sheet as strategic instrument.

At the same time, Ottawa has made it clear that Canada intends to be a long‑term, democratic supplier of energy to a more fragmented world, backing oil, gas, LNG, critical minerals and nuclear with state capital in a way that would have been politically unthinkable a decade ago. This is not just another fiscal update. It is a reboot of how Canada thinks about wealth, risk and energy security.

So: is this genuine nation‑building, or is it balance‑sheet theatre – a sophisticated way to rename risk as wealth?

That question deserves a serious, comparative answer – not from inside Canada’s political narrative, but from the outside: from Norway, Singapore, Ireland and Kuwait. Because sovereign wealth, like most things in macroeconomics, is defined by its hardware, not its headlines.

Carney is the first Canadian prime minister in the modern era to arrive in office without a single day of prior elected experience. Former Governor of the Bank of Canada, then the Bank of England, then one of the world’s most prominent voices on climate finance, his entire brand was built on a proposition: I understand how the global financial system works, and I will bring that literacy to the job of running a country.

One year in, the polls suggest Canadians have largely accepted that proposition – but on his terms. He scores highest where technocratic competence is most visible: managing Donald Trump’s trade pressure, diversifying Canada’s export relationships, meeting NATO’s 2% of GDP defence commitment. He scores weakest where the kitchen table is closest: the cost of living and housing affordability. A prime minister elected to manage global turbulence is now being judged on whether his macro‑level architecture translates into grocery bills, rent and mortgage payments.

The Spring Update and the Canada Strong Fund land directly in that credibility gap. A sovereign wealth fund is the ultimate “macro” instrument. It sits uncomfortably in a political moment where voters are asking much blunter questions: why is my mortgage higher, why are groceries expensive, and why is my kid still priced out of housing?

The Canada Strong Fund: announcement vs hardware

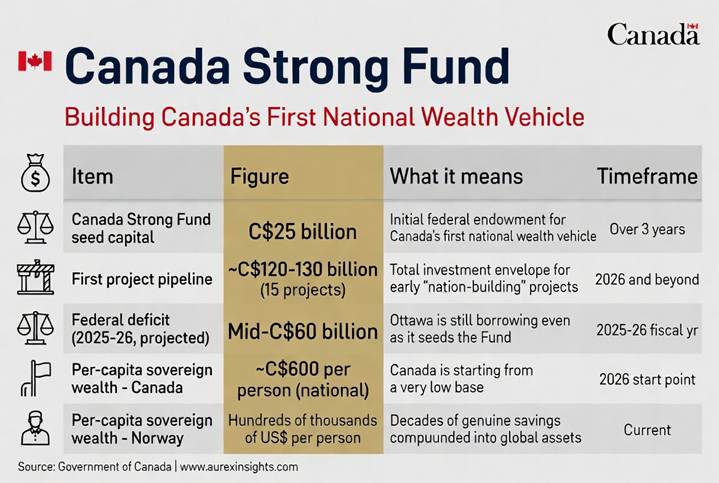

On paper, the Canada Strong Fund is a C$25 billion national vehicle that will invest in Canadian companies and projects across clean and conventional energy, critical minerals, agriculture and infrastructure, operating as a Crown corporation alongside private co‑investors. A retail investment product is promised, allowing ordinary Canadians to buy units and share in returns. It is being sold as “Canada’s first sovereign wealth fund” and explicitly compared with Norway.

The comparison is flattering – and dangerous – because it cuts both ways.

At the hardware level, four questions will determine whether this becomes real public wealth or a sophisticated relabelling of risk.

1. What is actually funding it?

The Spring Economic Update projects a deficit in the mid‑sixty‑billion range for 2025‑26, an improvement of roughly eleven billion over last fall’s budget, with modestly shrinking deficits beyond that but no rapid return to balance. In that world, a C$25‑billion fund seeded from general revenues is not a pot of spare cash. It is a conscious choice to borrow, then call the borrowed capital “savings”. Buying a financial asset with money you actually saved raises your net worth; buying it with a matching new loan simply changes the composition of your balance sheet.

2. Is it a wealth fund or a development bank?

A vehicle that co‑invests in politically salient domestic sectors – energy corridors, minerals, housing‑adjacent infrastructure – is far closer to a development bank or industrial policy arm than a classical, globally diversified sovereign wealth fund. That can be entirely legitimate; Singapore’s Temasek operates on exactly this model. But we should name it honestly. Calling a development bank a “wealth fund” confuses voters and obscures accountability.

3. Who holds the downside?

When the state co‑invests to “unlock” projects that struggle to attract private capital on their own merits, it typically absorbs below‑market risk pricing. Private partners capture a disproportionate share of the upside; the public sector carries the exposure. Canada has created a buffet of such vehicles over the past decade – from the Canada Infrastructure Bank to the Canada Growth Fund and Indigenous Loan Guarantees. The risk with the new Fund is that it simply adds one more layer to that stack, without ever forcing a clear distinction between who gets paid when things go well and who pays when things go wrong.

4. Where are the investment rules?

Norway’s Government Pension Fund Global is governed by explicit parliamentary rules: a strict external investment mandate, withdrawal limits tied to expected real returns, and disciplined ethical guidelines. By contrast, the Canada Strong Fund’s mandate, structure and deal framework are described as “to be confirmed in the coming months”. In an institution like this, the governance is the product. Without it, the rest is branding.

Canada will only get a real wealth fund if it is honest about where the money comes from, what risks it takes, and how returns flow back to citizens.

A day after the Prime Minister’s announcement, Ottawa filled in more of the hardware. The Canada Strong Fund will be seeded with C$25 billion in government capital deployed over three years on a cash basis, operating as a Crown corporation at arm’s length from government under an independent board and chief executive. It will lean heavily on projects already moving through the federal system – from the Major Projects Office to existing infrastructure, energy, mining and advanced manufacturing programs – and, crucially, will act primarily as a minority equity investor through shares, partnership and trust interests, and warrants rather than as a lender of last resort. That makes it a complement to Ottawa’s existing constellation of debt‑focused vehicles – the Canada Infrastructure Bank, Export Development Canada, the Business Development Bank and the Indigenous Loan Guarantee Corporation – rather than a replacement. The political logic is straightforward: where federal policy, regulatory support and capital help get nation‑building projects across the finish line, taxpayers should capture a share of the resulting commercial returns, not simply underwrite private gains. Whether the Fund delivers on that promise will turn on execution, deal selection and how genuinely arm’s‑length it proves to be from its political sponsors.

Why the Canada Strong Fund matters: Energy security and state capital

The Canada Strong Fund is not a neutral pool of savings. It is being launched in a world where energy security has become the defining economic and geopolitical question of the next decade. The war in Iran has pushed oil prices higher, disrupted transport routes and exported inflation into every oil‑importing economy. US tariffs are reshaping global trade patterns. Central banks, including the Bank of Canada, are holding policy rates while watching energy‑driven inflation risks with unusual intensity.

In that world, the countries that can deliver large volumes of reliable energy under the rule of law will shape the new map. Canada’s initial project pipeline – roughly fifteen major projects, with a combined investment envelope commonly described in the C$120-C$130 billion range – makes the intent explicit. Alongside critical minerals and infrastructure, the Fund will sit in a wider policy architecture that backs oil, gas, LNG export infrastructure, pipelines and nuclear capacity.

This is not a hedge. It is a deliberate decision to use the federal balance sheet to de‑risk long‑cycle energy projects that private markets will not fund on their own, and to position Canada as the long‑term supplier when Gulf stability and authoritarian producers look less reliable. State capital is being used not just to “crowd in” private money, but to anchor an energy strategy.

That dual purpose is precisely why the Fund’s design matters so much. A vehicle that takes on concentrated, long‑dated energy risk must either be run to true commercial standards, or it becomes a slow‑burn fiscal backstop for projects that cannot stand without political support. The line between sovereign wealth and sovereign exposure is thin.

Nova Scotia offers a glimpse of the strategy on the ground. Recent offshore oil and gas bids in the hundreds of millions of dollars, backed by experienced global operators, are being framed not just as resource plays but as pillars of an Atlantic energy hub, sitting alongside offshore wind and onshore gas. The province is not waiting for federal direction; it is positioning itself as a cornerstone supplier in a more fragmented global market, with the promise of jobs, service contracts and revenue for hospitals, roads and community services.

That is what the Canada Strong Fund is supposed to enable at national scale: translating abstract state risk‑taking into concrete local projects and pay‑cheques. But the same logic reinforces the need for discipline. When federal capital is deployed into complex, long‑cycle energy infrastructure that depends on durable policy support, it becomes even more important to show, line by line, how much risk taxpayers are carrying and what return they are actually earning.

What good looks like: Norway and Singapore

Norway’s Government Pension Fund Global is the canonical benchmark – and worth understanding precisely. The Fund was built from genuine fiscal surpluses, not from borrowing. Transfers began only after Norway’s budget moved into sustained surplus in the mid‑1990s, following a recession and banking crisis. The state got its fiscal house in order first, then layered real oil surpluses into a global investment portfolio.

Today, the Fund holds well over two trillion US dollars in assets, roughly three times mainland Norwegian GDP. On a per‑citizen basis, that is hundreds of thousands of dollars in financial wealth. Crucially, the Fund invests almost entirely abroad, to avoid overheating the domestic economy and creating the “Dutch Disease” it was designed to prevent. The principle is simple: if you buy a financial asset with money you actually saved, your net worth rises; if you buy it with a matching loan, your net worth is unchanged. Norway did the first. That is why its wealth is real.

Singapore’s Temasek points to a different, but equally coherent, model: a state‑owned investment company that holds long‑term equity stakes in strategic sectors, operates commercially and pays a material dividend back into the government budget each year. Temasek is industrial policy with a balance sheet – and it works because it is genuinely commercially disciplined. Stakes are recycled. Returns are real. Losses are publicly acknowledged.

Both models share one non‑negotiable feature: they generate actual, measurable returns back to the state, governed by rules insulated from short‑term political pressure.

The Kuwait reality check: seventy years of foregone wealth

Here is a number that should make every Canadian policymaker uncomfortable.

Kuwait – a country smaller than New Jersey, with a population of about four million – has been converting oil revenues into sovereign capital since 1953. Its main fund now holds roughly one trillion US dollars. Canada, with around forty‑one million people and the world’s fourth‑largest oil production, is launching its first national sovereign wealth fund in 2026 at C$25 billion – less than what some mid‑sized economies hold in foreign exchange reserves.

On a rough, per‑capita basis, Kuwait’s fund is worth a couple of hundred thousand US dollars per resident. Norway’s sits even higher. Canada’s starting point is in the low hundreds of dollars per person. The constitutional and market realities are different, but the compounding math is not. For seventy years, Canada treated resource revenue as income; Kuwait and Norway treated it as capital.

Starting at C$25 billion in 2026 is better than never starting. But it should be done with the humility of knowing how late we are – and with the rigour to do it right this time.

The Ireland warning: “borrow to save”

Ireland provides the most instructive cautionary tale.

Dublin is channelling a fraction of its extraordinary corporate tax windfalls – dominated by a handful of large US multinationals – into new long‑term funds. The political optics are excellent: Ireland is “saving for the future”. The underlying arithmetic is less reassuring. Roughly one euro in six of these windfall receipts is being saved; the rest is being absorbed into ongoing spending. The target fund sizes will be reached not only by diverting windfalls, but by borrowing tens of billions of euro by 2030.

“Borrow to save” creates an asset on one side of the balance sheet and new debt on the other. Net improvement depends entirely on whether investment returns outpace borrowing costs – a structurally uncertain bet, especially over long horizons in competitive global markets.

Ireland also faces a harder structural risk. Official fiscal and climate watchdogs estimate that missing binding 2030 climate targets could trigger compliance costs or emissions transfer payments measured in the high single‑digit to mid‑tens of billions of euro. Those are not abstract figures. They are potential future calls on the very fiscal capacity that is supposed to underpin the new savings funds. A cynic might observe that, if climate policy continues to undershoot, the funds may look less like intergenerational endowments and more like future EU compliance reserves. You cannot fix today’s under‑investment in climate action by borrowing to build a fund and hoping tomorrow’s bill never arrives.

Canada is not Ireland. It is a larger, more diversified economy, with its own currency and no Brussels‑style climate fines on the horizon. But the temptation to use sovereign wealth language to describe borrowed ambition exists on both sides of the Atlantic. The question for Canada is whether the Canada Strong Fund is funded from genuine surpluses in the years to come, or whether it becomes a borrowed asset quietly set against a borrowed liability.

The SME and digital gap: seven quarters and counting

The Spring Update does offer some real help for smaller firms. The cut in CPP premiums from 9.9% to 9.5% puts billions back into the pockets of workers and the payroll budgets of employers over the planning horizon. New apprenticeship grants and wage incentives for trades should make it easier for small companies to bring on and train staff. Making the Employee Ownership Trust tax exemption permanent is a sensible, long‑term reform that will give more owners a practical succession route and keep firms rooted in their communities.

Set against the broader picture, though, these are modest steps. Canada is still on course for a seventh straight quarter where more small businesses close than open. Business groups are blunt: large, government‑backed funds have come and gone in past budgets without shifting Canada’s underlying growth performance. There is a real risk that the Canada Strong Fund goes the same way if it is not carefully designed.

That matters because the real growth problem is no longer the absence of big announcements. It is weak productivity, slow adoption of digital tools, and a tax and regulatory system that makes it too hard to scale. The Fund is aimed mainly at physical assets and traditional sectors. The twenty‑first‑century challenge – raising productivity through technology, intangibles and better management in thousands of firms – remains only partially addressed.

In an economy where more small firms have closed than opened for nearly two years, the marginal dollar of risk capital arguably does more good inside a productivity‑raising software deployment in a 20‑person firm than in a ribbon‑cutting for a single megaproject. Unless the Fund’s architects deliberately carve out room for intangibles – software, skills, management – it will reinforce, rather than correct, Canada’s bias toward concrete over code.

Where Carney deserves credit

It is also important to say plainly what this government has got right in its first year. Mark Carney has been willing to treat Canada’s economic problems as structural, not cyclical – using the federal balance sheet and regulatory reform to change the country’s trajectory rather than merely steering through the next quarter. Budget 2025 put real weight behind that ambition: a productivity super‑deduction to cut the effective tax rate on new investment, enhanced innovation tax incentives, and a broader competition and consumer agenda intended to lower costs and spur innovation.

On housing, the government set a politically risky but economically necessary target of 500,000 completions per year over a decade, backed by tax changes for rental construction and a new Build Canada Homes delivery vehicle that is already approving projects on the ground. On trade and industrial structure, it has moved quickly to diversify beyond the United States, remove irritants in digital taxation ahead of CUSMA talks, and deploy targeted funds for critical minerals, Arctic infrastructure and tariff‑impacted regions. On affordability, it has paired one‑off relief measures with permanent changes to the tax mix, including cuts in middle‑income tax rates and relief for ordinary savers.

Seen in that light, the Canada Strong Fund and this Spring Update are not a one‑off flourish. They are the latest instalment in a coherent attempt to modernise Canada’s economic hardware: to combine more strategic use of the state’s balance sheet with a pro‑investment, pro‑innovation tax and regulatory framework. The question is not whether that ambition is welcome. It is. The question is whether the Fund’s eventual design will reinforce those gains by building genuine public wealth and supporting broad‑based business dynamism, or whether it will end up absorbing more risk than it creates in long‑term returns.

The verdict: wealth or re‑labelled risk?

One year in, Mark Carney is a more technically coherent and financially sophisticated prime minister than most of his predecessors. His government is genuinely thinking in balance‑sheet terms. The Canada Strong Fund – however incomplete its current design – represents the first serious attempt in Canadian history to build a national public wealth vehicle, rather than simply managing a rolling deficit.

But sophistication is not the same as strength, and ambition is not the same as discipline.

The test for any sovereign wealth fund is brutally simple: is it built from genuine savings, and does it earn a disciplined, transparent return that flows back to citizens through the budget? Everything else – nation‑building language, retail products, glossy project lists – is decoration. Funds work when they are financed honestly, governed tightly and forced to admit their losses. They fail – or become expensive exercises in socialising risk – when they are used to de‑risk projects that cannot attract private capital on their own merits, or when the asset is, in substance, a borrowed exposure set against a borrowed liability.

Canada is making a conscious choice to re‑enter the global energy game as a builder and long‑term supplier, not just as a regulator. That is the right instinct in a world where energy security and strategic resilience are the new reserve currencies. But the fact that the Canada Strong Fund is underwriting long‑cycle energy and infrastructure projects does not relieve it of the basic sovereign wealth test. It still has to be financed honestly, governed rigorously and run in the interests of citizens, not as a quiet subsidy pool for whichever projects can assemble the best lobbyists.

Canada now faces a choice it has deferred for seventy years. Does the Canada Strong Fund become a genuine reservoir of public wealth and long‑run diversification – closer in spirit to Norway – or a more sophisticated vehicle for levering the state deeper into the sectors we already over‑rely on? Is Canada learning from Norway and Temasek, or drifting quietly toward a polished version of Ireland’s borrowed ambition?

In the Carney era, the federal balance sheet is the battleground. The details of this Fund will tell us, very quickly, whether we are building strength – or simply re‑labelling risk.

That answer is worth watching very closely.