Borrowing to save on the back of a fragile tax boom

Dr. Brian O’Donnell | Aurex Insights | April 2026

Ireland’s corporation‑tax dependence is now built into Ireland’s fiscal strategy. There is a simple way to describe the Government’s plan for Ireland’s corporation‑tax windfall: spend five out of every six euros and save the sixth. Between now and 2030, the State intends to use the vast bulk of record, highly concentrated CT receipts to finance higher day‑to‑day spending and permanent tax measures, while a much smaller share is earmarked for the Future Ireland Fund and the Infrastructure, Climate and Nature Fund.

Anyone who remembers the 2000s has seen this film before. Back then, it was stamp duty, VAT and other property‑related revenues that swelled the Exchequer; the culture was “spend it while we have it”, and the political system found it easier to build new programmes than to tackle the underlying structural problems in housing, health, productivity or the tax base itself. When the property boom ended, the State discovered that it had hard‑wired temporary revenues into permanent commitments.

In the wake of that crisis, safeguards were put in place to stop a repeat. The IMF and EU pushed for a stronger fiscal framework; the Irish Fiscal Advisory Council was established as an independent watchdog; and the new European rules, including the expenditure benchmark, were designed to restrain exactly the kind of windfall‑fuelled overspending that had proved so damaging.

Yet the State is now back in dangerously familiar territory. IFAC, the IMF and others have warned repeatedly about the scale and concentration of corporation‑tax receipts – three firms now account for roughly 46 per cent of the total – and have urged governments to treat a large part of the revenue as windfall, to broaden the tax base and to keep expenditure growth within sustainable limits. The current and previous governments have acknowledged those warnings and then chosen a path that spends most of the windfall anyway.

The consequence is that Ireland is quietly loading future decades with risk. By using exceptional revenues to build permanent spending and tax decisions today, while gross debt continues to rise and while the long‑term funds are sized modestly relative to the exposure, the State is making the 2030–2040 period almost certain to be tougher: less fiscal space, more pressure from ageing, climate and interest costs, and fewer easy options if corporation‑tax receipts disappoint.

This is the skeleton beneath the surplus. The question is not whether Ireland looks strong in 2026 – it clearly does – but whether the combination of corporation‑tax dependence, “borrowing to save” and a “spend it while we have it” political logic is setting up the next hard adjustment

The Skeleton Beneath the Surplus: The CT story

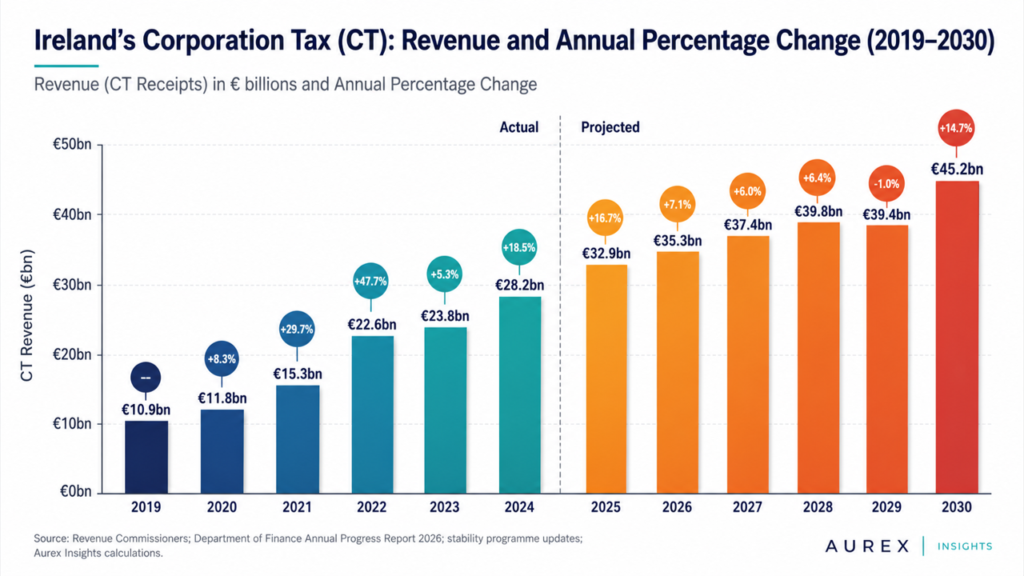

Ireland’s corporation-tax trajectory is extraordinary by any historical standard. Receipts rose from €10.9 billion in 2019 to €28.2 billion in 2024, are estimated at €32.9 billion in 2025 and are projected to reach €45.2 billion by 2030.

The key break came in 2022, when receipts jumped by 47.7 per cent in a single year. Many observers treated the slower growth recorded in 2023 as the start of a return to normality, but the Department’s latest projections point in the opposite direction: strong gains resumed in 2024 and 2025, with the tax base remaining structurally elevated across the rest of the decade. Link: (extension://efaidnbmnnnibpcajpcglclefindmkaj/https://assets.gov.ie/static/documents/ee08f522/Annual_Progress_Report_2026.pdf)

This is why the usual language of “temporary windfall” now looks incomplete. On the Department’s own numbers, the State is not cautiously stepping back from corporation-tax dependence; it is embedding that dependence more deeply into the fiscal model.

Dependence, not just growth

The most revealing figure is not the level of corporation-tax receipts but their share in the State’s ordinary income. On current projections, corporation tax accounts for 29.7 per cent of net current revenue in 2025, rises above 31 per cent in 2026 and 2027, reaches 32.0 per cent in 2028 and ends the decade at 32.9 per cent in 2030.

Put plainly, nearly one euro in every three used to fund day-to-day government activity is expected to come from corporation tax by the end of the decade. That is not a tax base becoming more balanced. It is a revenue system becoming more reliant on one of its most concentrated and least predictable pillars.

The official institutions that monitor Ireland’s fiscal position have repeatedly warned about that concentration. The Irish Fiscal Advisory Council has highlighted the growing dependence on a small number of firms, while Revenue’s own research continues to underline how unusually concentrated the tax is by taxpayer and sector.

The Skeleton Beneath the Surplus: The borrowing paradox

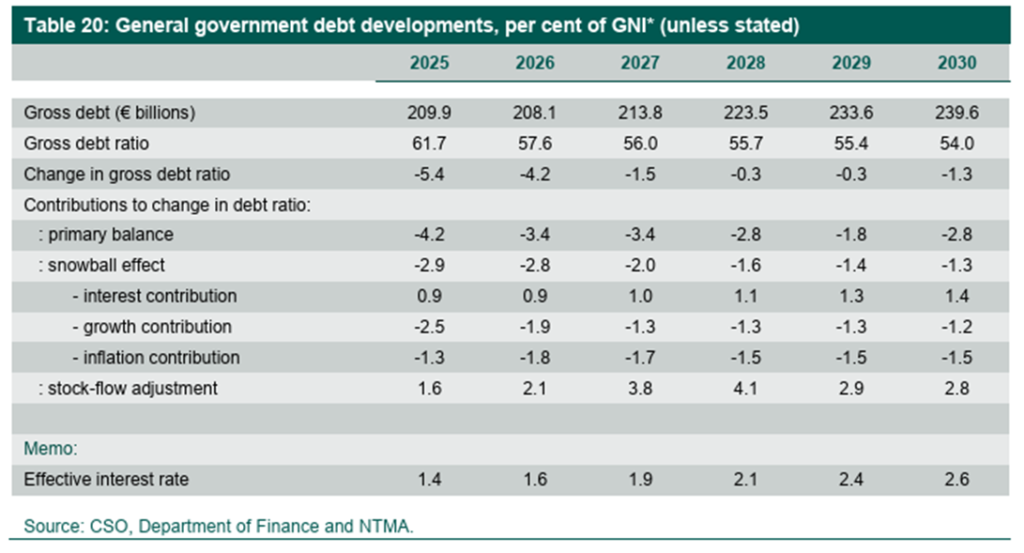

The headline debt story looks reassuring. Ireland’s debt‑to‑GNI* ratio is projected to fall from 61.7 per cent in 2025 to 54.0 per cent by 2030, while general government balances remain in surplus and the sovereign retains strong market access and AA‑category ratings.

But that headline masks a more awkward balance‑sheet story. As Table 20 in the Department of Finance’s Spring Annual Progress Report shows, gross general government debt stands at €209.9 billion in 2025 and is projected to rise to €239.6 billion by 2030, an increase of about €30 billion in cash terms even as the ratio falls. The same table records the effective interest rate on that debt rising from 1.4 per cent in 2025 to 2.6 per cent by 2030.

Table above – Rising debt, falling ratio: a simplified chart based on Table 20 shows gross debt climbing, the debt‑to‑GNI ratio drifting down and the effective interest rate edging higher over 2025–2030.*

The explanation lies in the arithmetic of debt dynamics. The ratio improves because nominal growth, inflation and primary surpluses are doing much of the work, not because the State is materially shrinking the nominal stock of debt. At the same time, the effective interest rate on that debt is projected to rise from 1.4 per cent in 2025 to 2.6 per cent by 2030, so Ireland ends the decade with more debt in cash terms and a more expensive average funding cost even though the headline ratio looks safer.

This matters because it is the backdrop to the Future Ireland Fund and the Infrastructure, Climate and Nature Fund. Those funds were established in 2024 legislation to convert part of today’s exceptional revenues into long‑term financial assets to help meet future ageing, climate and other pressures, with annual transfers planned through 2035 and combined assets potentially reaching around €100 billion by the mid‑2030s. The policy logic is understandable: save part of a volatile windfall while the money is available. The paradox is that the State is doing this while gross debt continues to rise and while the official EU debt metric does not net off the assets held in these funds against gross general government debt. In practice, that means part of the extra borrowing over the decade is not financing bridges, hospitals or current services in the usual way; it is financing the accumulation of financial assets in the Future Ireland Fund and ICNF. The State is, in effect, choosing to keep gross debt higher than it needs to be in order to build up investment funds whose value will move with the same global shocks that threaten corporation‑tax receipts in the first place.

In effect, Ireland is strengthening one part of the public balance sheet while asking markets to finance another at a rising average cost. In a near‑zero‑rate world that could look close to costless. In a higher‑rate world, it looks more like a carry trade that works only if long‑term fund returns comfortably exceed sovereign borrowing costs and if those assets can be mobilised when a corporation‑tax shock arrives. It is the fiscal equivalent of taking out a bigger mortgage at a higher rate to buy a portfolio of investments you hope will outperform – a strategy that works until markets or income disappoint.

The Skeleton Beneath the Surplus: Spending above the ceiling

A third structural issue sits beside the tax and debt story: the spending base is still growing quickly. Government expenditure growth ran at about 7.3 per cent in 2024, 6.9 per cent in 2025 and is planned at around 7.4 per cent in 2026, above the EU’s sustainable net expenditure benchmark of roughly 6.6 per cent for the period.

The Annual Progress Report also records a €700 million upward revision to the 2026 Exchequer Borrowing Requirement in the three months since the Stability Programme Update. That pattern matters because spending, once built into the system, is politically and administratively hard to reverse.

This is where the real fiscal risk lies. The most plausible stress scenario is not a sudden funding crisis but a slower squeeze: corporation-tax receipts fall back by several billion euro a year, while spending commitments built on today’s revenue base remain in place and the Government moves from surplus into structural deficit.

What Budget 2027 should confront

Ireland is not in fiscal crisis. By both historical and European standards, the public‑finance position in spring 2026 is strong, liquid and comparatively resilient.

But three structural features now sit beneath the reassuring headlines. Corporation‑tax dependence is deepening rather than moderating; gross debt is rising in cash terms even while the ratio falls; and spending growth is running above the level the EU framework treats as sustainable across the cycle. That mix leaves Ireland more, not less, exposed to a shock that hits multinationals, global tax rules or the cycle.

That is the real Budget 2027 debate. The central question is not whether Ireland has fiscal space today, but whether too much of that space rests on a narrow corporate‑tax base, optimistic debt optics and spending assumptions that will be hard to defend if the revenue cycle turns. If a recession, a multinational restructuring or a global tax shift knocks billions off corporation‑tax receipts, today’s strategy points towards the same pattern as the late 2000s: large, sudden deficits followed by painful consolidation.

The difference is that this time it would be even less defensible. The concentration of CT, the limits of “borrowing to save” and the risks of pro‑cyclical spending have been set out repeatedly by IFAC, the IMF and the European institutions; they are not hidden problems, and there is still time to use the windfall to build a more resilient tax base, a more disciplined spending system and an Ireland better prepared for the 2030s. If that opportunity is missed and the windfall is treated as permanent, the next downturn will not just be an economic shock – it will be a political reckoning for those who chose to ignore the warnings. The choice is stark: use the boom to fix the roof and the foundations now, or explain to voters in the 2030s why a once‑in‑a‑generation tax surge ended in another avoidable hard landing.

Dr. Brian O’Donnell is the founder and principal of Aurex Insights, an independent public policy, economic and legislative strategy practice working between Ireland and Canada.