The Locked-Out Generation

For many young adults in Ireland, homeownership has shifted from a realistic goal to an unachievable dream. Many remain living with their parents well into their late 20s and 30s, constrained not by choice but by soaring costs and limited options. Recent surveys reveal that 61% of young people aged 18-24 consider social housing alternatives, while only around 41% of first-time buyers manage to save an adequate deposit. This “locked-out” generation is facing a housing market that has spiraled decisively beyond reach for ordinary citizens.

Soaring Prices Deepen the Crisis

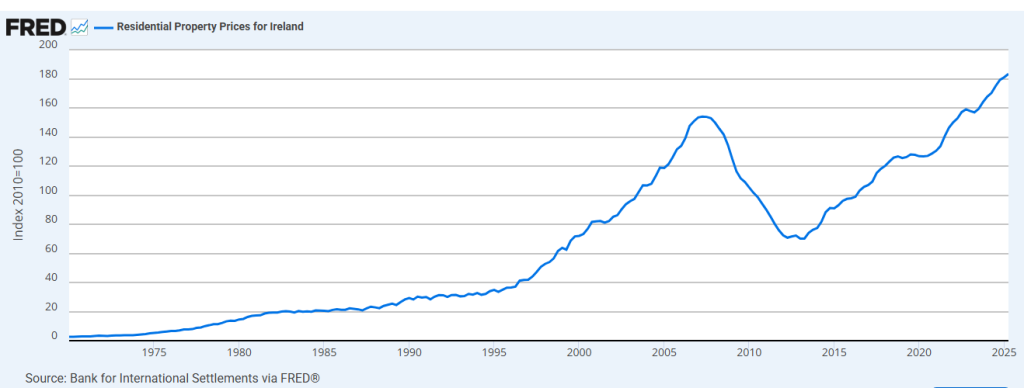

Data from the Federal Reserve Economic Data (FRED) highlights the Residential Property Price Index for Ireland hitting 183.3 in Q2 2025, an 83% increase since 2010 (base year 2010=100). According to the Central Statistics Office (CSO), residential property prices rose 7.5% in the year to July 2025. The national median house price is now approximately €375,000, while in Dublin, the median price stands near €490,000 – more than double the average annual income.

This relentless price escalation reflects decades of housing costs outpacing inflation and wage growth, pushing ownership further from reach and contributing to rising social inequality.

Ambitious Targets, Slow Progress

Ahead of the 2024 general election, the outgoing Fianna Fail/Fine Gael government committed to delivering 40,000 new homes in 2024 with plans to ramp up to 300,000 new homes by 2030 (an average of 60,000 annually in the new PfG). However, only 30,300 homes were completed in 2024, falling short of the target. Early 2025 data show some improvement with about 15,100 completions in the first half of the year – a 35% rise on Q2 2024 largely driven by apartment building.

Yet, even with this positive momentum, 2025 completions are forecasted to remain well below the government’s 41,000 homes target, indicating that despite progress, supply continues to seriously lag demand.

Barriers to Faster Housing Delivery

Multiple structural obstacles hamper supply-side progress:

- Lengthy planning delays and cumbersome bureaucracy delay timeline and deter investment.

- Increasing development levies and fees inflate upfront costs, paradoxically pushing sale prices higher.

- Scarce land availability, especially around Dublin and other key growth areas, hikes acquisition costs.

- Rising labor and material costs squeeze developer margins, slowing new projects.

- Access to affordable financing remains limited, constraining investment particularly in affordable and rental sectors.

The Economic and Social Research Institute (ESRI) warns that no major supply jump is expected in 2025 or 2026, reinforcing the urgent need for systemic reform to meet housing demand.

Policy Gaps Risk Further Price Increases

Government efforts such as the “Housing for All” plan, levy waivers, and infrastructure investment have so far been insufficient to reverse supply deficits. Planning reforms remain slow and fragmented, and regulations continue to create an unpredictable development landscape. Notably, some (many) policies unintentionally raise costs that developers pass onto buyers and renters, fueling a cycle where delay intensifies scarcity and prices rise further.

The Human and Economic Toll

- Young adults delay moving out and forming families, with serious social consequences.

- Homelessness peaked at roughly 15,747 people in mid-2025, a record high by official counts.

- Rising housing costs influence emigration decisions, with about one-third of Irish residents considering leaving the country due to affordability pressures.

- Persistent housing challenges exacerbate inequality and impair labor market flexibility, threatening Ireland’s economic vitality and growth prospects.

A Call for Radical, Coordinated Action

To begin reversing this crisis, Ireland urgently requires:

- Radically streamlined and centralized planning and permit procedures to cut years from project timelines.

- Prompt release and activation of public land for affordable housing and rental developments.

- More focused direct subsidies and targeted incentives, particularly for purpose-built rental housing.

- Innovation in modular, scalable construction techniques to reduce costs and accelerate delivery.

- Tightened controls on speculative investments and land banking to stabilize prices.

- Stronger intergovernmental cooperation to ensure policies translate into real housing outputs.

What’s Next: A Canadian Housing Market Comparative

Over the coming weeks, Aurex Insights will deliver an in-depth comparative analysis of Canada’s housing market. With soaring rental demand, stalled new home construction, and ambitious government programs underway, Canada faces its own set of challenges and opportunities. This detailed exploration will highlight lessons on supply strategies, affordability, and policy innovation from both sides of the Atlantic.

Stay Connected

Follow Aurex Insights on LinkedIn and Twitter/X for ongoing expert insights.