By Dr. Brian O’Donnell | Founder & Principal Consultant, Aurex Insights | March 2026

Everyone is watching Brent. Far fewer people are watching their electricity bill.

That distinction matters – because the most consequential economic impact of the Iran conflict for Irish households and businesses may not arrive at the petrol pump. It may arrive quietly, and with a lag, through a winter electricity bill.

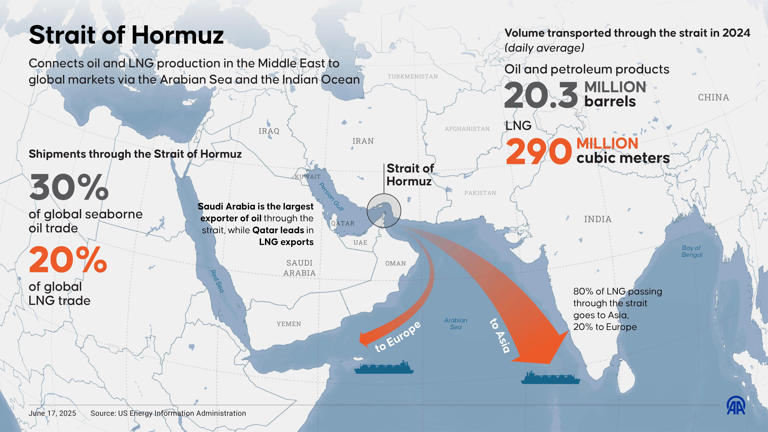

The Strait carries 30% of global seaborne oil trade and 20% of global LNG trade daily. Qatar leads LNG exports through the route. With 80% of LNG flows destined for Asia, any disruption forces Asian and European buyers into direct competition for alternative cargoes – transmitting the shock immediately into European gas benchmarks like TTF.

Source: US Energy Information Administration

The Oil Story: Serious, But Buffered

Oxford Economics’ latest analysis of the Iran conflict draws a critical line between oil and gas markets. Their base case assumes a moderate disruption to the Strait of Hormuz – roughly 4 million barrels per day of oil supply affected on average over the coming quarter. That is a serious shock. But with spare capacity available in Saudi Arabia and the UAE, rebuilt global inventories, and flexible US shale production able to respond relatively quickly, Oxford sees Brent averaging in the high-$70s in Q2 – approximately $15 above their pre-conflict path, but well short of a full-blown oil crisis.

This is disruption, not Armageddon. Broadly, I share that central view on oil. A Brent in the high-$70s is painful at the margins – it slows disinflation, nudges headline inflation higher, and keeps central banks slightly more cautious than markets might prefer – but it is not a 1970s-style rupture.

There is, however, a legitimate question about what consumers are actually paying at the pump – and why. Retail petrol and diesel prices are not simply a function of the crude barrel price. They incorporate refining margins, distribution costs, retailer markups, and excise duties that do not move symmetrically with oil. The well-documented “rockets and feathers” dynamic – where pump prices rise quickly when crude rises but fall slowly when crude falls – means that in practice, consumers routinely pay above what the underlying barrel movement strictly justifies. This asymmetry is compounded by the forward purchasing strategies of major fuel retailers, who hedge a significant proportion of their supply needs in advance. A retailer that locked in supply at pre-conflict prices and is now passing on spot-equivalent increases to consumers is not absorbing a cost shock – it is capturing a margin windfall. Irish and European regulators have previously flagged this pattern during energy price surges. It warrants close scrutiny now. The pain at the pump, in other words, may reflect not just geopolitical reality but also the absence of adequate price transparency and regulatory oversight in retail fuel markets.

The gas story is different. And for Ireland, it is the one that matters most.

The Gas Story: No Alternative Route, No Buffer

Qatar is the world’s second-largest LNG exporter. Unlike oil, Qatari gas has no alternative export route that bypasses the Strait of Hormuz. When the Strait is disrupted, Qatari LNG is disrupted – and there is no Saudi spare capacity equivalent to absorb the shortfall.

The market has already responded decisively. By close of trading on 2 March, the TTF front-month contract – the benchmark European gas price, based in the Netherlands – was up 36% from pre-weekend levels, having traded nearly 50% higher intraday. That places it among the largest single-session moves in European gas markets over the past year. By early afternoon on 3 March, TTF was trading at approximately €57 ($66) per MWh – a further 28% above the previous day’s settlement. This is not a forecast. It is already in the price.

Oxford’s baseline sees key benchmarks – TTF and the Asian JKM price – settling at around $14 USD/MMBtu, roughly 30% above their February baseline. The impact is expected to persist longer than any oil shock, because Europe must refill gas storage ahead of next winter. Asian buyers, simultaneously locked out of Qatari supply, compete directly with European buyers for available cargoes. The squeeze is structural, not transient.

Why Ireland Is Uniquely Exposed

The transmission from European gas markets into national electricity prices is not uniform – it depends critically on each country’s reliance on gas-fired power generation.

The cross-country data at 2 March market close is instructive. Front-month wholesale power contracts rose 19.5% in the UK – where gas accounts for approximately 35% of generation – and 13.5% in Italy, where gas accounts for around 41%. Germany, with a lower gas share of approximately 13%, saw a more moderate rise of 7.4%. France, where gas accounts for just 3% of the generation mix, actually fell 14% on 2 March – reflecting short-term positioning dynamics – before rebounding 16% the following day as structural logic reasserted itself.

Ireland sits at the extreme end of this spectrum. According to Gas Networks Ireland, gas generated 47% of Ireland’s electricity in 2023, with wind contributing 39% and other sources making up the balance. On that structural basis, Ireland’s wholesale electricity sensitivity to TTF movements is at least comparable to – and potentially exceeds – the UK and Italian experience. Of the countries examined, Ireland has the highest structural gas dependency in its power mix.

This is not an abstract market observation. It means that every significant move in European gas benchmarks is transmitted, with relatively little attenuation, directly into Irish wholesale electricity prices – and, with a lag, into household and business energy bills.

The Hedging Lag: Why Relief Takes Longer Than the Headlines Suggest

There is a further dimension that most market commentary misses: the hedging cycle.

Irish electricity suppliers hedge a large share of their expected winter demand through forward purchases and long-term contracts. A sustained period of elevated TTF through spring and summer does not simply disappear if spot prices ease next January. It is baked into the forward contracts already being priced and rolled – embedding today’s geopolitical shock into the tariffs that will shape next winter’s bills, regardless of where spot prices sit at that point.

We saw this mechanism operate with painful clarity during the 2022–23 gas shock. European benchmark prices collapsed long before households saw any meaningful relief in their electricity statements. The structural mechanism that produced that lag remains fully intact today. Higher TTF levels lift forward power curves in gas-exposed markets, and Irish suppliers – operating in one of Europe’s most gas-intensive systems – are price-takers in that dynamic.

My Assessment: Under-Appreciated Gas Risk

My base case is a temporary but non-trivial gas-led squeeze: European gas prices remaining roughly 20–30% above their pre-Iran trajectory for several months, as Qatari exports are disrupted and Asian and European buyers compete for available cargoes. That is sufficient to slow disinflation materially, nudge euro-area inflation several tenths higher, and keep the ECB slightly more cautious on the pace of rate cuts than markets currently anticipate.

For Ireland, the consequences are very concrete. A gas-driven rise in wholesale power costs would hit households and SMEs precisely at the moment many had begun to believe the worst of the energy crisis was behind them. Another period of elevated TTF filtering into 2026 and 2027 tariffs would re-open cost-of-living pressures, squeeze real incomes, and return energy to the centre of political debate – even if petrol and diesel prices never approach the levels implied by a true oil crisis.

Where I think markets are under-pricing risk is not on oil – it is on the social, political, and inflation consequences of a gas-driven power squeeze in import-dependent, gas-intensive economies like Ireland.

The Longer-Term Policy Dimension

There is a structural silver lining – though it is cold comfort in the short term. Episodes of sharp LNG-driven price volatility structurally improve the economics of renewable generation, lifting forward power prices and revenue expectations for wind and solar projects. For Ireland, which has set ambitious offshore wind targets, a sustained period of elevated gas prices perversely accelerates the investment case for the very infrastructure that would reduce this vulnerability over time.

The policy lesson is not simply to manage the current shock. It is to use its political salience to lock in the infrastructure decisions – grid investment, storage capacity, accelerated offshore wind – that durably reduce Ireland’s exposure to the next one.

In the short term, the Irish government should also revisit the case for a real-time retail fuel price monitoring mechanism – similar to those operating in Australia and parts of continental Europe – to ensure that any pass-through of wholesale cost increases to consumers reflects actual cost exposure rather than opportunistic margin expansion. If forward hedging has insulated retailers from the current shock, consumers should not be absorbing spot-equivalent price increases. That is not market economics – it is extraction.

The Bottom Line

TTF is already up 50% intraday from pre-conflict levels. German front-month power is up 31%. Ireland, with the highest gas dependency in the European comparison set, has no structural buffer equivalent to France’s nuclear fleet or Germany’s diversified mix.

Markets may be right not to price a full oil crisis. The question is whether Irish households, businesses, and policymakers are positioned for a gas crisis that – unlike the catastrophe everyone feared – is already arriving quietly, and will make itself felt not at the forecourt, but on next winter’s electricity bill.

Are we aiming our policy and market responses at the right target?

Aurex Insights provides independent economic, public policy, and strategic advisory services. Dr. Brian O’Donnell, DBA is available for media comment, policy briefings, and consulting engagements at brian@aurexinsights.com | www.aurexinsights.com