Published by Dr. Brian O’Donnell | Aurex Insights | March 2026

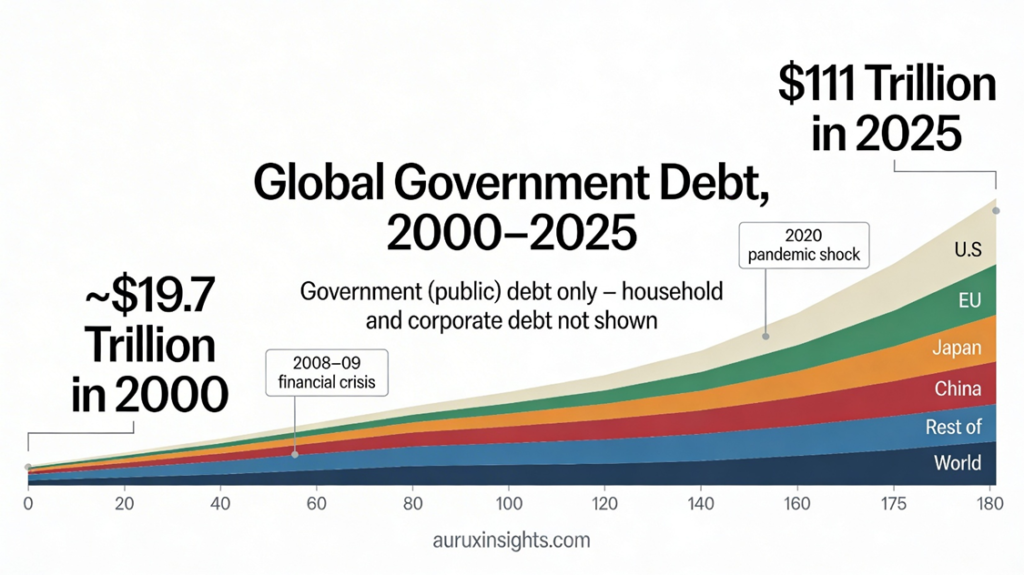

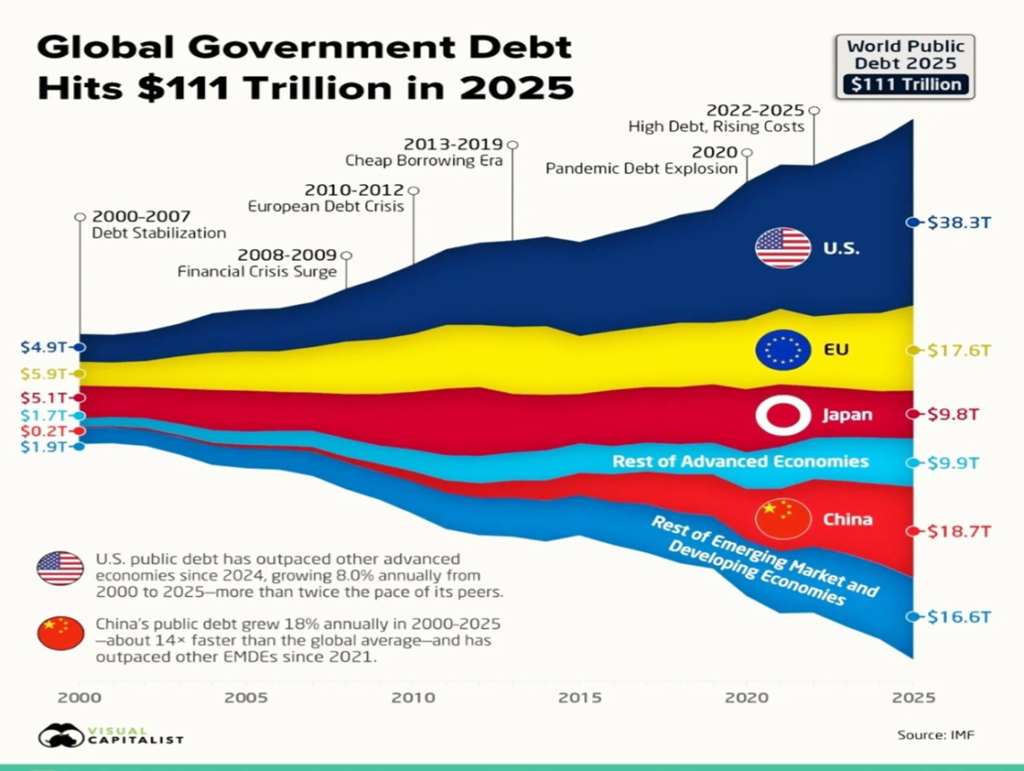

Global public debt has just crossed 111 trillion dollars. Between 2000 and 2025, government debt worldwide rose more than five‑fold, from about 19.7 trillion to 111 trillion, with the steepest jumps after the 2008 financial crisis and the 2020 pandemic. The usual reaction is alarm: we’re told governments have “lived beyond their means” and must now tighten belts.

That diagnosis is wrong. We do not live in a world that ran out of money. We live in a world where, every time the system breaks, leaders reach for the public balance sheet. A sovereign government that issues its own currency can always create the financial resources to stabilise a crisis; the hard limits are real capacity, institutional design, and political will, not keystrokes at the central bank. For countries that do not control their own currency – such as Eurozone members – the constraint bites earlier through funding and institutional limits rather than pure monetary sovereignty. Global bond markets have absorbed this surge in public and corporate borrowing so far, but that resilience rests on increasingly fragile foundations: large rollover needs, shifting investor bases, and tighter financial conditions.

What the debt chart really shows

The chart tracks gross government debt, not household or corporate liabilities, and breaks the last quarter‑century into distinct phases: “debt stabilization” before 2008, a post‑crisis surge, the Eurozone debt episode, a “cheap borrowing” era, the pandemic spike, and then a period of high debt and rising interest costs. Each phase lines up with a crisis or regime shift.

In the early 2000s, public debt grew broadly in line with global GDP, rising from 19.7 to 35.8 trillion dollars. Beneath the surface, private credit was doing the real lifting, fuelling housing booms across advanced economies.

The 2008 – 09 financial crisis triggered a sharp jump in sovereign borrowing as governments bailed out banks and launched stimulus programmes; global public debt leapt from 35.8 trillion to 45.5 trillion in two years.

The Eurozone debt crisis then pushed EU government debt higher again before subsequent austerity measures slowed the rise.

From 2013 to 2019, ultra‑low interest rates allowed governments to maintain higher debt loads with relatively low servicing costs, as global public debt drifted from about 60.7 to 73.9 trillion.

In 2020, the pandemic drove the largest one‑year increase on record, with global public debt jumping from 73.9 trillion to 84.9 trillion dollars.

Since 2022, debt has remained high while the cost of servicing it has risen, especially for the U.S. and many emerging economies, as policy rates reset upwards.

The pattern is not overspending in good times; it is emergency spending in bad times. Each shock -financial, fiscal, or epidemiological – has been met first with balance‑sheet tools: deficits, guarantees, quantitative easing, liquidity backstops. That is the hallmark of a modern monetary regime.

An equation for our era

To see what this means for inflation, housing, and living standards, it helps to formalise the logic in a simple way:

Here, \(FD\) is fiscal deficits: net government spending that adds financial assets to the private sector. \(CG\) is credit growth: banks expanding balance sheets, especially through mortgage and corporate lending. \(SC\) is structural constraints: housing supply, land and planning rules, energy systems, labour capacity, and infrastructure.

In plain language, price pressures are driven by three forces: how much net financial power the state injects, how much the private sector leverages that through credit, and how tight the real constraints are in the economy. If you push \(FD\) and \(CG\) hard while leaving \(SC\) largely untouched, you should expect rising debt, rising asset prices, and persistent affordability problems.

From homes to balance sheets

Housing is where this equation becomes personal. In the 1970s and early 1980s, a typical salary in countries like Ireland, the UK or Canada could often buy a modest home at roughly two to three times annual income; today, in many urban markets, entry‑level homes are priced closer to seven to nine times average earnings. (Exact ratios vary by city and data source, but the direction and scale of change are clear across major Anglophone markets.) The shift is not trivial; it represents a structural reclassification of housing from a basic consumption good to a leveraged financial asset.

The last 25 years of policy explain much of that change. Before 2008, credit‑fuelled housing booms were tolerated as growth engines. After the crash, public balance sheets were used to rescue financial institutions and stabilise demand, but housing supply, land policy and taxation were only marginally reformed. In the 2010s, austerity constrained public investment, while low interest rates and abundant liquidity inflated asset values. The pandemic then delivered a final stress test: massive deficits protected incomes, but collided with pre‑existing bottlenecks in housing, logistics and energy.

The outcome: households face a world where both public and private balance sheets have expanded, yet buying or renting a home has become dramatically harder.

Sophisticated tools, lazy policymaking

Modern monetary theory has often been caricatured as a licence for unlimited spending. Its core insight is more sober: a sovereign currency issuer faces a real‑resource constraint, not a financial one. The limit is not whether the state can credit bank accounts; it is whether the economy has enough labour, capital, land and technology to absorb that spending without generating damaging inflation.

What the global government‑debt chart reveals is not that governments ignored this; it is that they responded to crises with the fastest, least politically costly tools available. Deficits and central bank operations can be deployed in days. Structural reforms to housing, energy, competition, skills, or state capacity take years and create clear winners and losers.

We have, in effect, built a regime of sophisticated balance‑sheet management paired with remarkably lazy policymaking. Every major shock gets a financial patch; the deeper design problems are deferred. In advanced economies, most new issuance is simply rolling yesterday’s promises: for OECD governments in 2026, roughly four‑fifths of new borrowing will refinance existing debt rather than fund new programmes, illustrating how legacy stocks now shape fiscal choices.

The real constraint: capacity and design

If we treat the 111 trillion figure as evidence of irresponsibility, the logical response is more austerity and less investment. That would be a mistake. The real challenge is to change what we do with the state’s fiscal and monetary capacity, not to pretend that capacity doesn’t exist.

A more productive agenda would involve three shifts:

- Use fiscal power to expand real supply. Target deficits at the binding constraints: housing, climate‑safe energy, resilient infrastructure, and care. That means sustained public investment, reformed planning and land policy, and partnerships that crowd in long‑term private capital rather than just supporting asset prices.

- Tackle distribution and rent‑seeking head‑on. Every unit of public debt is an asset on a private balance sheet. Tax and regulatory policy should minimise unearned windfalls in land and monopoly sectors, support deep, well‑regulated capital markets rather than periodic bailouts, and ensure that new public liabilities translate into broad‑based improvements in living standards, not just higher valuations.

- Stop treating crises as excuses to avoid reform. When the next shock arrives – as it will -stabilising incomes and credit is essential. But those measures should be tied to explicit structural programmes: large‑scale housing initiatives, energy system redesign, productivity‑enhancing reforms in health and education. Emergency money should buy transformation, not simply time.

The global government‑debt “explosion” is not a morality tale about households and governments sharing the same budget constraint. It is a political‑economy story about how we choose to use the uniquely powerful balance sheet of the modern state. The danger is not that we have spent too much in the abstract; it is that we have repeatedly spent without solving the problems that matter most. Every major shock gets a financial patch; governments then quietly shelve the harder work of fixing the underlying design failures.

The task for this decade is not to shrink the chart at any cost, but to align our balance‑sheet reflexes with a serious programme of structural renewal. Only then will the trillions already created show up not just in bond markets and house prices, but in the lived reality of affordable homes, resilient systems, and rising real incomes.

About Aurex Insights

Aurex Insights provides independent economic, public policy, and strategic advisory services. Dr. Brian O’Donnell, DBA, works with public, private, and non‑profit clients on economic analysis and strategy. Contact: brian@aurexinsights.com | www.aurexinsights.com